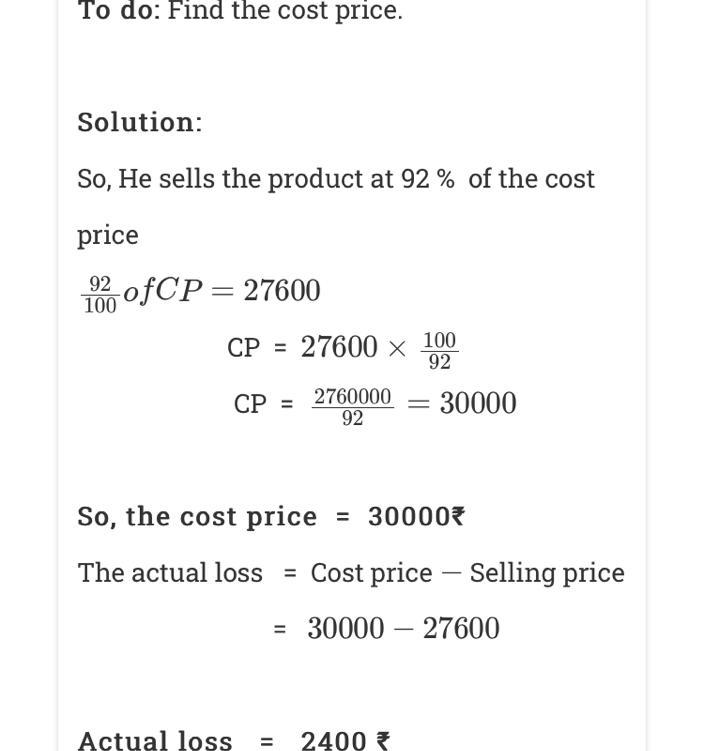

Therefore the cp answer is 30000

Hope this help let me know if you question

Answer:

COGS= $7,950

Explanation:

Giving the following information:

Beginning inventory 10 units at $120

First purchase 15 units at $150

Second purchase 30 units at $180

Third purchase 20 units at $195

Helen Tools has 25 hammers on hand at the end of the year.

<u>Under the FIFO method of inventory cost, the cost of goods sold is calculated using the purchasing price of the first units incorporated.</u>

We need to calculate the number of units sold:

Units sold= total units - ending inventory

Units sold= 75 - 25= 50 units

COGS= 10*120 + 15*150 + 25*180= $7,950

Answer:

6.974% and 4.218%

Explanation:

The computation is shown below:

Here we use the 52-week low stock price

The Highest dividend yield is

= Dividend ÷ Stock price

= 2.39 ÷ 34.27

= 6.974%

The Lowest dividend yield is

= Dividend ÷ Stock price

= 2.39 ÷ 56.66

= 4.218%

We simply applied the above formula so that we can determine highest and lowest dividend yield

Moral judgment is typically intuitive rather than in-deathly reflective in the ethical decision-making model.

What is decision making?

Identifying decisions and gathering information to make choices is referred to as "decision making" in this context.

The moral judgements give insight on a person's organization, society, and personality. The principles of decision-making can be influenced by a person's ethical ideals and actions.

As a result, the ethical decision-making model is moral judgment.

Learn more about on decision making, here:

brainly.com/question/13129093

#SPJ1

The answer is D. I had this question before