Answer:

Answer for the question:

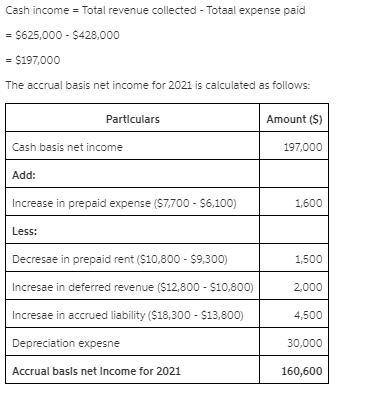

Haskins and Jones, Attorneys-at-Law, maintains its books on a cash basis. During 2021, the law firm collected $610,000 for services rendered to its clients and paid out $425,000 in expenses. You are able to determine the following information about accounts receivable, prepaid expenses, deferred service revenue, and accrued liabilities: January 1, 2021 December 31, 2021 Accounts receivable $ 75,000 $ 67,000 Prepaid insurance 5,800 7,100 Prepaid rent 10,500 9,600 Deferred service revenue 10,500 12,200 Accrued liabilities (for various expenses) 13,500 17,700 In addition, 2021 depreciation expense on office equipment is $28,500. Required: Determine accrual basis net income for 2021.

is given in the attachment.

Explanation:

Answer:

the correct answer is C. A trading or pricing structure that interferes with efficient buying and selling of securities.

Explanation:

Answer: There will be an effect as there might be labor shortage.

Explanation: Minimum wage is the least renumeration pay that can legally be paid by employers to their workers. It is a price floor method below which employees can't sell their labor. When a minimum wage is imposed by the government, firms are not allowed to pay less than the wage rate mandated by the government.

If the minimum wage is set below the equilibrium wage rate, quantity of labor reduces in comparison to the quantity demanded by employers. If the least paid person is paid $16 per hour and the government imposes a minimum wage of $10, There will be a shortage of labor because most people won't like to work as a result of the lower income. It also leads to lack of motivation among workers.

As a result of Consumer Confidence Index rising, spending in the economy will increase and aggregate demand will rise.

Consumer Confidence Index (CCI) refers to how optimistic people are about their finances. When the CCI is high:

- People are more confident in their finances and the ability to make income in future

- People will spend more in the economy because they are more confident in their income

- Aggregate demand will rise as more people demand goods and services

If the CNN is correct in reporting that the CCI is rising, we can expect that spending in the economy will rise and so will aggregate demand.

In conclusion, spending in the economy will increase and aggregate demand will rise.

<em>Find out more at brainly.com/question/9930012. </em>

,Answer: a. 9,450 units

Explanation:

You need to find the weighted average contribution margin for both products.

Product A

Weighted average contribution margin = Contribution margin * Units sold / Total units sold

= 34 * 7,600 / (7,600 + 2,400)

= $25.84

Product B

= 59 * 2,400 / 10,000

= $14.16

Breakeven point in units = Fixed costs/ (Weighted average contribution margin of both A and B)

= 378,000 / (25.84 + 14.16)

= 9,450 units