Answer:

Requirement 1 :

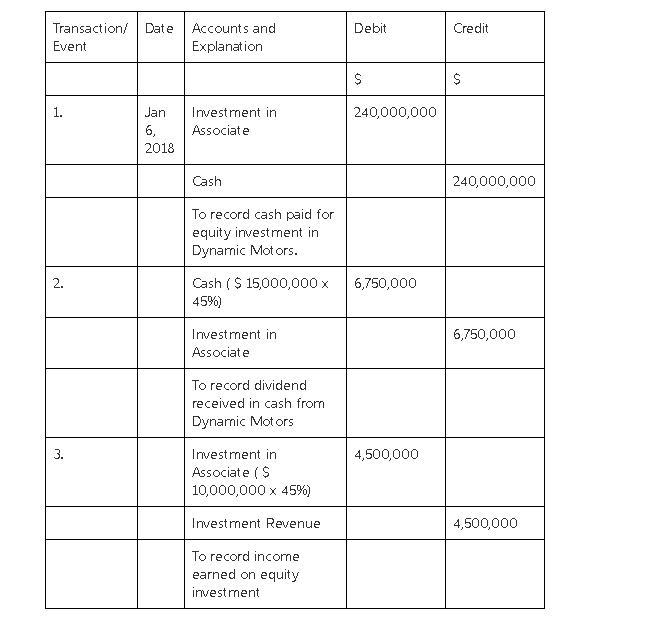

Excel Motors should use the Equity method to account for its investment in Dynamic Motors, because the investment results in significant influence over the invested company.

Requirement 2 :

In the books of Excel Motors:

[ Kindly find the attachment ]

Answer:

The correct answer is option B.

Explanation:

The Cost of Property is given at $ 216,000

.

The MACRS rates are 0.2, 0.32 and 0.192 for years 1 to 3 respectively.

Depreciation for the year 1 will be

= $216,000*0.2

= $43,200

Depreciation for the year 2 will be

=$216,000*0.32

=$69,120

Total Depreciation for the year 1 and 2 will be

=$43,200+$69,120

=$112,320

The book value of this equipment at the end of year 2

=$216,000-$112,320

=$103,680

On checking the above value with Answer B that is

=$216,000*(1-0.2-0.32)

=$216,000*0.48

=$103,680

Answer:

B

Explanation:

A. the same amount to every investor regardless of their desired rate of return.

B. the present value of the future income which the stock generates.

C. an amount computed as the next annual dividend divided by the market rate of return.

D. the same amount as any other stock that pays the same current dividendand has the same required rate of return.

the dividend models are used to determine the value of a stock. It is assumed that the value of the stock is equal to the present value of the cash flows or dividends of the stock

The intrinsic value of a stock can be calculated using various dividend models. some of dividend growth models include:

1. The Gordon constant growth dividend model

2. The two-stage dividend growth model

3. The H-model

4. The three-stage dividend growth model

For example, if the dividend of a share in year 1 and 2 is 50 respectively and the discount rate is 10, the present value of the firm =

50 / (1.1) + 50 / (1.1^2) = 86.78

False. indirect is not direct .

Answer:

The quality of social service delivery in South Africa is very poor.

Explanation:

The quality of service may be poor due to several factors such as the manipulation of politicians, no accountability of work done, not enough workforce employed to do the necessary job, unprepared in terms of planning, failure to cope up with change in the dynamic environment etc.

The social service delivery can be improved by understanding the needs of the market, handling the information better, hiring better and qualified workforce, updating and implementing policies to cope up with change and provide time in planning the service delivery.