Answer and Explanation:

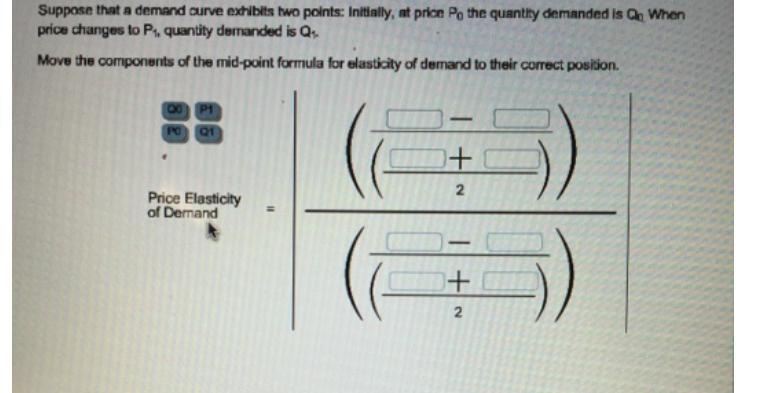

The formula to compute the price elasticity of demand is as follows:

= Percentage change in quantity demanded ÷ percentage change in price

At Price P0, the Quantity demanded is Q0

And,

At Price P1, the Quantity Demanded is Q1

Just like this, it could be computed

divided by

divided by

Answer:

Items of Cash : Cash and Till float

Risks : Fraud and Theft

Controls : Segregation of duties over the receipt and recording of money and Every cashier should only be responsible for his own funds.

Test of Controls : Do a surprise cash count and Enquire about and observe the controls over cash by management

Explanation:

Bank and cash transactions occur on a daily basis in all businesses. Although the cash and bank balances may not individually be significant, annually the volume of cash and payment transactions and bank deposits can be significant to the entity.

Items of Cash

Cash balances comprise the following:

Risks

Cash is highly susceptible to fraud and theft by employees, often in collusion with third parties.

To mitigate this risk related to cash balances, management will usually implement strict control policies and procedures for cash handling and recording.

Controls in the bank and cash cycle can be divided into 2 categories:

Basic Controls

- Segregation of duties over the receipt and recording of money.

- Different forms of cash (sales, petty cash, cash loans) should be kept separately and recorded separately.

- Proper stationery control. Receipts, cash sales slips/invoices must be numerically recorded

- Safeguarding of money. Cash must be locked in a Volt and deposited as soon as possible. You would also need control over the key to the Volt.

Control over Cash

- Cashier must balance cash on a daily basis and must compare it with the source documents (receipt, cash invoices, cash register totals) and record it on a cash receipt summary. The Cash Receipt Summary must be Signed by the Cashier, Independently reviewed by the Senior Official.

- Every cashier should only be responsible for his own funds. Usually during lunch. Cash registers must be locked away.

- Every cashier should be responsible for his own float. They should lock in Cash Drawer.

- Supervision over cashiers. Through the use of Cameras.

- Cash must be banked as soon as possible.

Audit approach for testing these accounts

- Enquire about and observe the controls over cash by management.

- Do a surprise cash count (also attend on a surprise basis the daily balancing of cash). In the presence of a Cashier who signs back of the receipt, agree the cash with the supporting documentation (receipts, cash invoices, cash register total) and follow the float through to the balance in the ledger.

- At a later stage follow the cash counted through to deposit slip, and agree it with the cash counted, ensure they are banked timeously and follow the total of the deposit slip through to the cash book and bank statement.

The allowance for doubtful accounts credited, instead of accounts receivable when recording the adjusting entry for bad debts Because accounts receivable is made up of numerous client accounts, it cannot be credited unless it is known which particular customer will not pay.

The provision for questionable accounts is referred to as a "counter asset" since it reduces the value of an asset, in this example, the accounts receivable. The compensation, often known as a doubtful account, is management's projection of the amount of accounts receivable that customers will not pay. Let's assume, using the aforementioned example, that on June 30 a business reports an accounts receivable debit balance of $1,000,000. The business predicts that $50,000 will not be converted into cash and expects some consumers won't be able to pay the full amount.

learn more about doubtful account visit brainly.com/question/28944789

#SPJ4

<span>The principle of opportunity cost is that the economic cost of using a factor of production is the alternative use of that factor that is given up.

</span> This principle is used as a measure to choose one economic choice and investment, either financial or capital, over another with the goal to <span>ensure that scarce resources are used efficiently.</span>

Answer:

Items a) and b)

a) items used currently in the production of goods to be sold items

b) held for resale items currently in production for future

Explanation:

Inventory consists of current assets to be used in production of final goods or are the ones which are final goods and held for sale.

In the given case also, statement a includes raw materials, which are used to make the final good to be sold, which is a part of inventory.

Further, statement b includes work in production or final goods which are currently in production but would be resold.

The items which are kept for their use as like machinery or furniture or which shall be disposed are not inventory but are in fixed assets category.