The correct option is B. In this type of economy the government has total control over allocation of all resources. <span />

Answer:

-$7,621

Explanation:

Calculation to determine the net present value of the machine

Using this formula

Net present value of the machine=(Net cash flow *present value of an annuity at 11%)- Amount invested

Let plug in the formula

Net present value of the machine=($2,800+$26000*2.4437)-$78,000

Net present value of the machine=($28,800*2.4437)-78,000

Net present value of the machine=$70,379-$78,000

Net present value of the machine=-$7,621

Therefore the Net present value of the machine is -$7,621

In a situation when managers must analyze data from 500 hotels to determine when to discount rooms based on occupancy patterns they are facing with the following challenge: they need to analyze large amounts of information in the decision-making process in order to make the correct decision. The goal of the decision <span> is to gain competitive advantage.</span>

Answer:

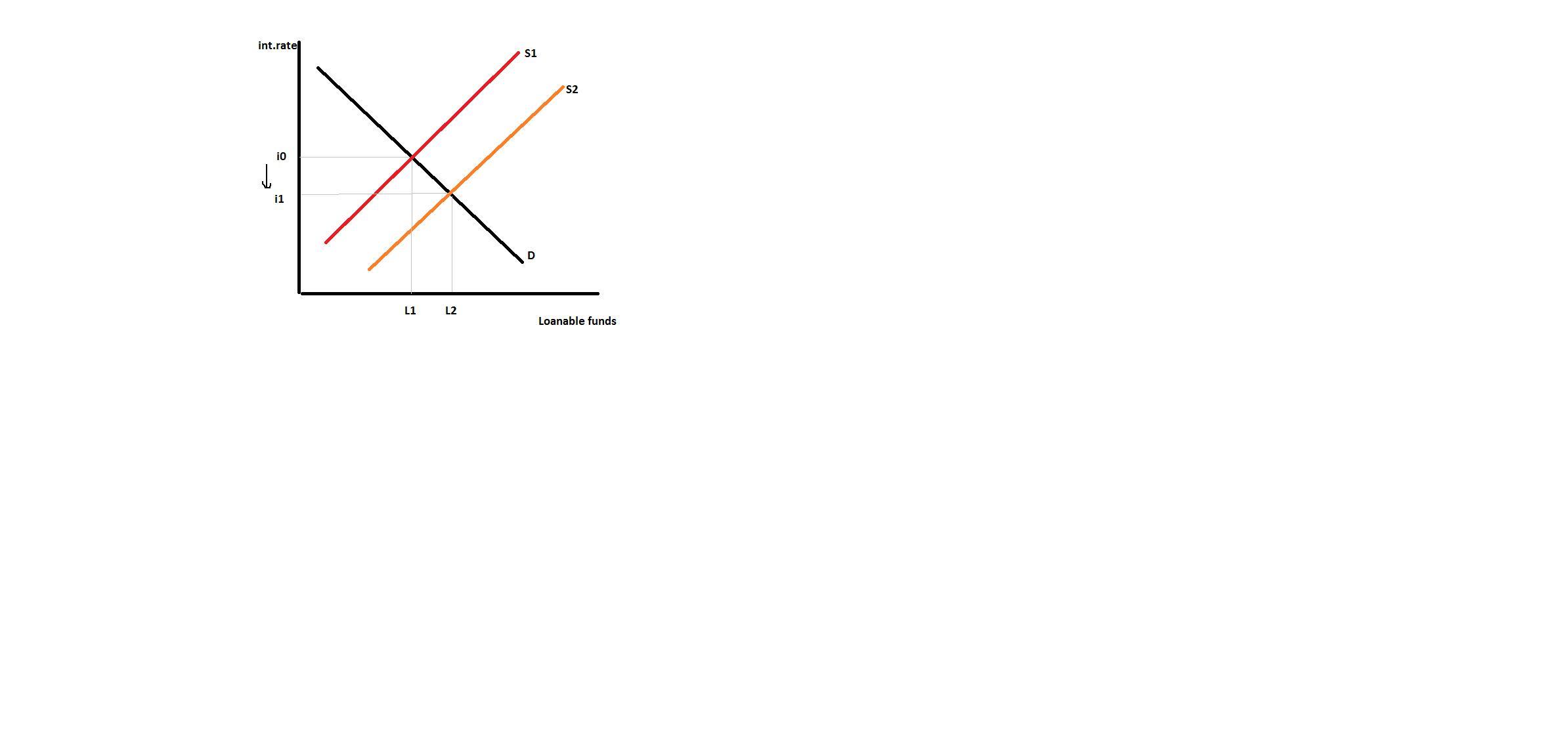

1. Decrease, increase

2. Supply curve shifts to the right

3. NCO will rise

4. Real exchange rate falls and net exports rises

Explanation:

Fiscal deficit occurs when government spending's exceed government revenue. When the government lowers its export subsidies while keeping other spending's and taxes unchanged, it leads to a fall in the fiscal deficit.

1. However, the reduction in expenditure on export subsidies <em>decreases</em> the fiscal deficit, thereby <em>increases </em>public savings.

2. As public savings increase it leads to an increase in funds available to be loaned out. So the <em>supply curve</em> for loanable funds will <em>shift to the right</em> from S1 to S2. This will lead to a <em>fall</em> in the interest rate.

3. As we know that net capital outflow is inversely related to the interest rate. A fall in the interest rate above will lead to a <em>rise</em> in net capital outflow.

4. When net capital outflow increases, people move funds out of the country. Thus, supply of dollars will increase. While demand for dollars has remained unchanged, it leads to a<em> fall</em> in the real exchange rate. As exchange rate falls, the equilibrium level of net exports will <em>rise</em>.

Foundation. Motivation represents "those psycholigical proccesses that cause the arousal,direction, and persistence of voluntary actions that are goal directed."