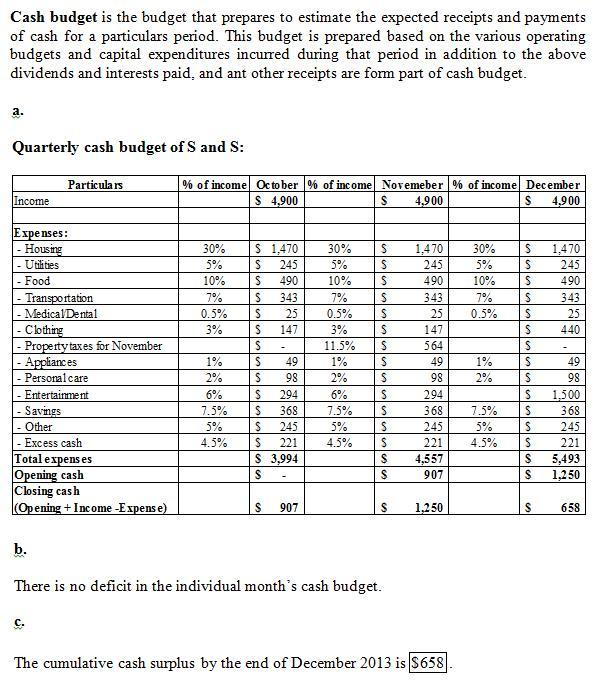

Answer

The answer and procedures of the exercise are attached in the following archives.

Explanation

You will find the procedures, formulas or necessary explanations in the archive attached below. If you have any question ask and I will aclare your doubts kindly.

Answer:

(B) expands on the information in the applicant's resume.

Explanation:

Interview is an expands on the information in the applicant's resume.

Screening interview: It is conducted to to eliminate applicant, who does not meet the minimum requirement of the company. These interview save time and cost of companies by eliminating under qualified or skilled candidates. This is a process to determine whether the candidate can move further for interview or not.

Hiring interview: It is a type of interview, where qualified candidate appear after taking different selection process, in this interview, hiring manager want to understand whether is good fit for the position. It is generally conducted one to one.

Applicant can be well prepared if he or she know what to expect in the interview.

Answer:

Casey can buy 50 pound of fish and 30 pounds of shrimp.

Explanation:

you divide 150 by 3 and you get 50. For shrimp you divide 150 by 5 and you get 30.

Answer:

The answer is A

Explanation:

Competitive environment is an environment where competitors compete with one another for customers.

For example, Westpac, NAB, Commonwealth Bank and ANZ are in the same competitive environment. These are banks in Australia.

Types of competition are perfect competition, monopoly, monopolistic competition, oligopoly etc.