Answer: Cash flow from financing activities (CFF) is a section of a company's cash flow statement, which shows the net flows of cash that are used to fund the company. Financing activities include transactions involving debt, equity, and dividends.

Explanation:

Answer:

B. No, approval by an individual other than the requestor establishes greater accountability over inventory.

Explanation:

This step is required as it will ensure control over inventory usage.

<span>part of a contractionary fiscal policy</span>

Non-organic food is cheaper, and often has brand names, which appeal to the consumer more than an organic brand does.

Answer:

Explanation:

worker's production rate = 60/3 = 20units per hour

monthly capacity 160 x 20 = 3200 units.

capacity needed to produce 2000000 units

= 2000000/3200

= 625

therefore, since they already have 500 workers, they need to hire 125 more workers.

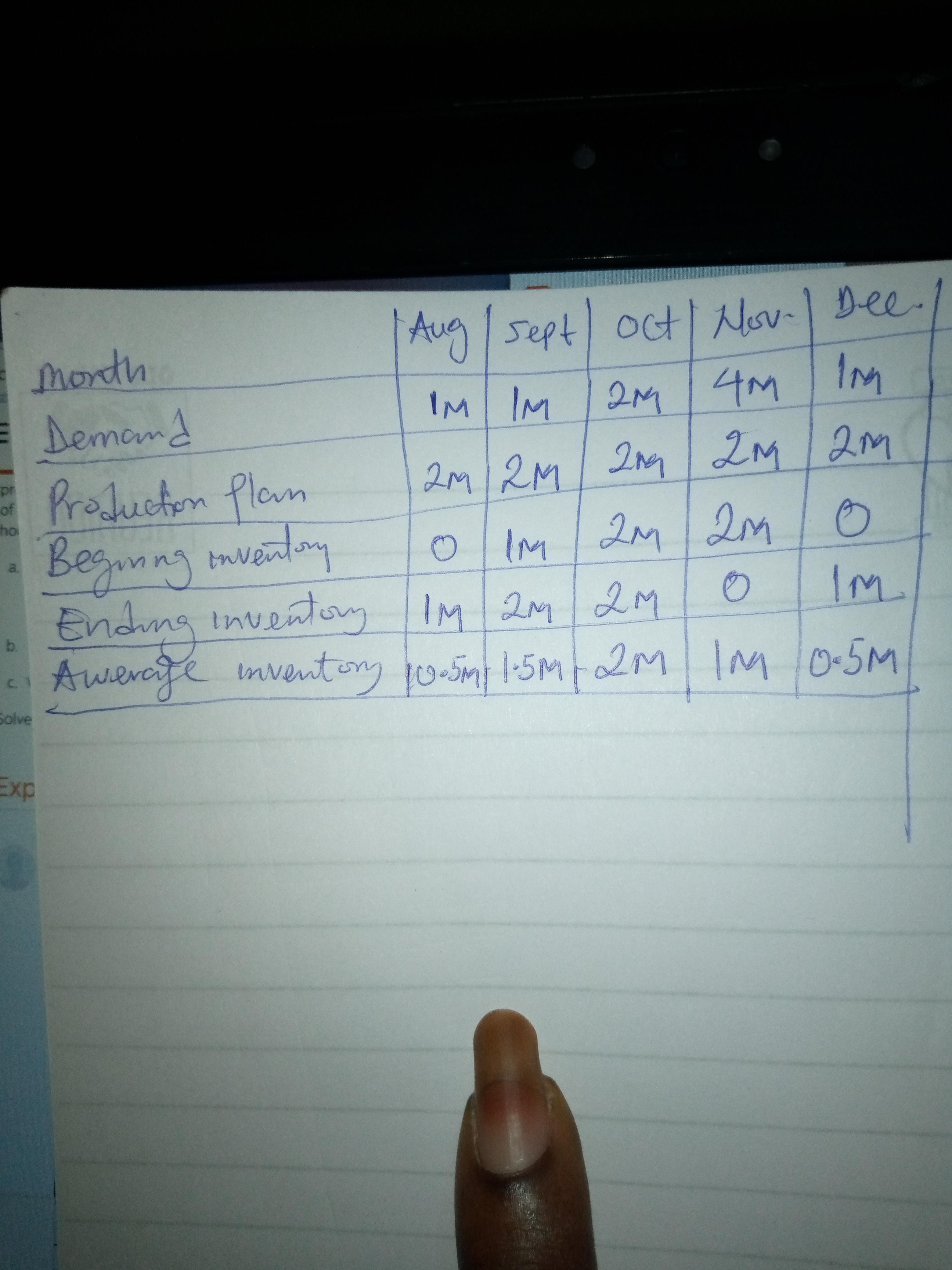

b) At the end of October they will have 2 million inventory.

c) Average inventory in each of the months has been listed in the attachment below.